Umbrella Insurance: The Cheapest Way to Add Millions in Coverage (And Why Most People Are Dangerously Unprotected)

Imagine this: You’re hosting a backyard barbecue. A guest slips on your wet patio, breaks their hip, and sues you for $750,000 in medical bills and lost wages. Your homeowner’s insurance covers only $300,000. That leaves **you** on the hook for $450,000—draining your savings, threatening your home, and even putting future wages at risk.

Now imagine that scenario costs you **less than $20 per month** to prevent.

That’s the shocking power of umbrella insurance—and most people don’t even know it exists.

In a world where lawsuits are rising at an alarming rate (nearly 40 million civil lawsuits filed annually in the U.S., according to the National Center for State Courts), skipping umbrella coverage isn’t just risky—it’s financially reckless. Yet fewer than 15% of homeowners carry it, often because they assume it’s expensive, unnecessary, or only for the wealthy.

Spoiler: **It’s none of those things.**

In fact, umbrella insurance is one of the most overlooked financial safety nets in personal finance—a single policy that can add **$1 million to $5 million** in liability protection for pennies a day. And once you understand how it works, you’ll wonder why you didn’t get it yesterday.

Let’s break down exactly how to get maximum protection for minimum cost—and why waiting could be the most expensive mistake you ever make.

—

What Exactly Is Umbrella Insurance (And Why Should You Care)?

Umbrella insurance is **extra liability coverage** that kicks in when your standard policies—like auto or homeowner’s insurance—hit their limits. Think of it as a financial force field that shields your assets, income, and future from catastrophic claims.

Unlike regular insurance, which caps payouts at $100K–$500K, umbrella policies start at **$1 million** and can go up to $10 million or more. And here’s the kicker: the average annual cost is just $150–$300—less than a streaming subscription.

But why do you need it?

Because modern life is litigious. Dog bites, car accidents, slip-and-falls, even social media defamation claims can spiral into six- or seven-figure lawsuits. According to a 2024 report by the Insurance Information Institute, the average bodily injury liability claim now exceeds $20,000, while severe accidents routinely surpass $100K. Without umbrella coverage, **you’re personally liable for every dollar beyond your base policy limits**.

Dr. Marcus Chen, a risk management professor at Columbia University, puts it bluntly:

“Umbrella insurance isn’t a luxury—it’s a necessity for anyone with assets, income, or dependents. One lawsuit can erase decades of financial progress. For less than $1 a day, you can sleep soundly knowing your family’s future is protected.”

—

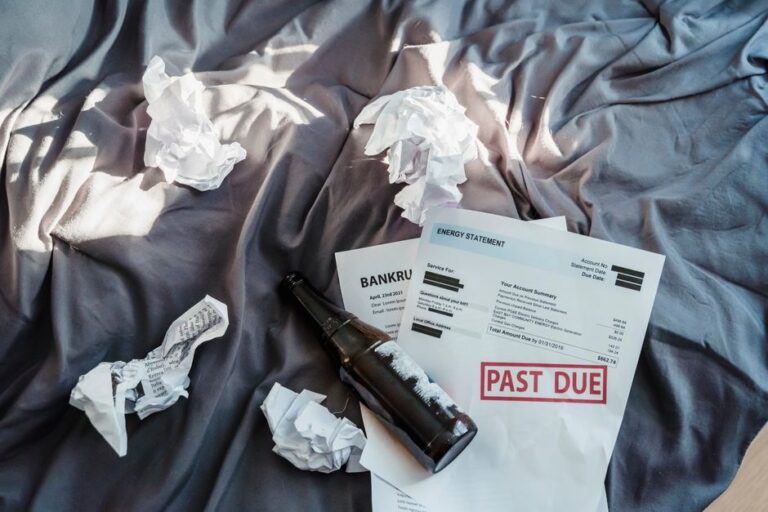

The $500 Mistake That Cost a Family Their Home

Meet Sarah and Jake, a middle-income couple from Austin, Texas. They owned a modest home, drove safe cars, and had solid auto and homeowner’s policies. They thought they were covered.

Then their teenage son hosted a party while they were away. A guest fell down the basement stairs, suffered a traumatic brain injury, and sued for $1.2 million in damages.

Their homeowner’s policy capped at $300,000. Their auto policy didn’t apply. Suddenly, Sarah and Jake faced a $900,000 judgment. Their savings? $45,000. Their retirement? Frozen. Their home? At risk of forced sale.

“We had no idea one accident could destroy everything,” Sarah later told a local news outlet. “If we’d known about umbrella insurance, we’d have paid $18 a month and avoided this nightmare.”

Their story isn’t rare. The U.S. Department of Justice reports that over 60% of personal injury lawsuits result in judgments exceeding $50,000. And without umbrella coverage, families like Sarah’s are left financially exposed.

—

How to Get $1 Million in Coverage for Less Than Your Gym Membership

Here’s the secret most agents won’t tell you: **umbrella insurance is dirt cheap—if you bundle it**. Most insurers require you to carry underlying policies (like auto or home) with them first. But once you do, adding umbrella coverage is shockingly affordable.

Let’s compare real-world pricing:

| Provider | Annual Premium | Coverage Amount | Cost Per Day | Bundling Discount |

|---|---|---|---|---|

| State Farm | $168 | $1M | $0.46 | Up to 20% off auto/home |

| Allstate | $220 | $1M | $0.60 | 15% multi-policy savings |

| GEICO | $150 | $1M | $0.41 | 10% discount with auto policy |

| Liberty Mutual | $195 | $1M | $0.53 | Up to 25% off total premiums |

As you can see, the cheapest option costs just $0.41 per day—less than a cup of coffee. And bundling often saves you even more on your existing policies.

But here’s the counter-intuitive truth: the wealthier you are, the more you need umbrella insurance—but the less it costs relative to your risk. High-net-worth individuals pay slightly more, but their exposure is exponentially greater. For everyone else, it’s pure financial leverage.

—

3 Myths Keeping You Dangerously Underinsured

Let’s bust the biggest lies that stop people from getting protected:

Myth #1: “I don’t have enough assets to need it.”

Reality: Even if you don’t own a home, your **future wages** can be garnished. Creditors can seize bank accounts, tax refunds, even retirement funds. Umbrella insurance protects your earning potential—not just what you own today. Myth #2: “My auto/home policy covers everything.”

Reality: Standard policies have strict limits. A single serious accident can blow past those caps in seconds. Umbrella coverage is your backup when the first line of defense fails. Myth #3: “It’s only for rich people.”

Reality: Anyone with a car, a dog, a pool, a social media presence, or a teenager is at risk. Lawsuits don’t discriminate by income—and neither does umbrella insurance. — Most people associate umbrella insurance with car accidents. But today’s liability landscape is far broader: – **Dog bites**: Over 4.5 million occur annually in the U.S., with average claims exceeding $50,000. In 2023, a Florida man was ordered to pay $1.8 million after his teenage daughter posted a defamatory TikTok video. His homeowner’s policy covered only $100,000. Without umbrella insurance, he lost his boat, his savings, and nearly his house. This is the new normal. And it’s not going away. — You don’t need a financial advisor. You don’t need to overhaul your life. Just follow these steps: 1. **Call your current auto/home insurer**. Ask: “What’s your rate for a $1M umbrella policy?” Most will quote instantly. Pro tip: Ask about “excess liability” vs. “umbrella”. True umbrella policies cover broader risks (like libel or slander), while excess liability only extends your base policies. Always choose umbrella. — Here’s the uncomfortable truth: insurance companies don’t profit from people who never file claims. They profit from people who think “it won’t happen to me.” But consider this: Umbrella insurance isn’t about fear. It’s about **freedom**. Freedom to host parties, let your kids drive, walk your dog, or post online—without lying awake wondering if one mistake will bankrupt you. And at less than $1 a day, the cost of inaction is infinitely higher than the cost of protection. — Most $1M policies cost between $150 and $300 per year—roughly $0.40 to $0.80 per day. Rates vary by state, coverage amount, and bundling discounts. Yes! Renters can be sued for injuries in their unit, pet incidents, or even online behavior. Many insurers offer standalone umbrella policies for renters. It covers liabilities beyond your base policy limits—including libel, slander, false arrest, and certain lawsuits not included in home or auto policies. Some insurers allow it if you have renter’s or auto insurance with them. Always confirm underwriting requirements before applying. Generally, no—unless you own rental property or use your home for business. Consult a tax professional for your specific situation. — If this post opened your eyes to how easy—and essential—it is to protect your family with umbrella insurance, **share it with someone you love**. Tag a friend who drives, owns a home, or has kids. Because the best time to get coverage was yesterday. The second-best time is right now.

The Hidden Risks You’re Not Thinking About

– **Slip-and-fall injuries**: Property owners are liable for unsafe conditions—even on rented land.

– **Social media**: Defamation, invasion of privacy, or cyberbullying claims are rising sharply.

– **Teen drivers**: Your child’s mistake could become your financial ruin.

– **Rental properties**: If you rent out a room or vacation home, your exposure multiplies.How to Get the Cheapest Umbrella Insurance in 5 Minutes

2. **Bundle everything**. Keeping all policies with one carrier unlocks the biggest discounts.

3. **Increase underlying limits first**. Insurers require minimums (e.g., $300K liability on auto). Bump those up slightly—it’s cheap and necessary.

4. **Compare quotes online**. Use sites like Policygenius or NerdWallet to cross-check rates.

5. **Buy before you need it**. Once a claim is filed, you can’t add coverage retroactively.Why Waiting Could Cost You Everything

– 1 in 3 Americans will be sued in their lifetime (American Bar Association).

– The average time from accident to lawsuit filing? Just 14 months.

– Once a claim is reported, your insurer may drop you—or raise rates by 30%.FAQ

How much does umbrella insurance cost?

Do I need umbrella insurance if I rent?

What does umbrella insurance cover that regular policies don’t?

Can I get umbrella insurance without homeowner’s insurance?

Is umbrella insurance tax-deductible?