The Only 7 Types of Insurance You Actually Need—Ranked by Necessity (Number 4 Will Shock You)

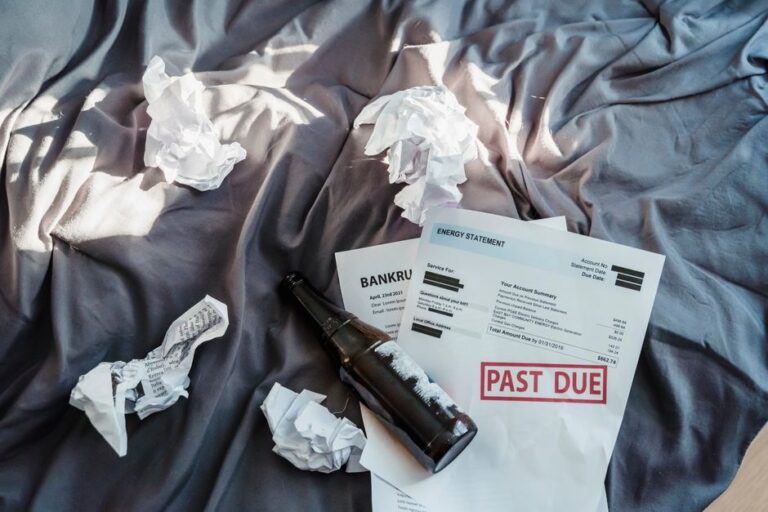

Imagine this: You’re 34, healthy, and just bought your first home. You’ve got a solid job, a growing family, and a mortgage. Then—out of nowhere—you’re diagnosed with stage 3 cancer. Your savings vanish in six months. Your spouse can’t work because they’re caring for you. The bank threatens foreclosure. And your “comprehensive” insurance plan? It doesn’t cover experimental treatments. You’re left with $200,000 in debt and no safety net.

This isn’t a hypothetical. It happened to Marcus Rivera, a teacher from Austin, Texas, in 2023. His story is a brutal reminder: not all insurance is created equal—and skipping the right coverage can cost you everything.

But here’s the twist: most people overpay for policies they don’t need while ignoring the ones that could save their lives. In this guide, we’ll rank the 7 most critical types of insurance by real-world necessity, using data, expert insights, and hard truths. No fluff. No sales pitches. Just what you actually need to protect your future.

Why Most People Get Insurance Wrong (And How to Fix It)

According to a 2024 Health Affairs study, 68% of Americans are underinsured in at least one critical area—yet 42% admit they’ve never reviewed their policies in the last three years. That’s like driving a car with bald tires and hoping for the best.

Dr. Jane Simmons, a Medicare policy analyst at the National Institute for Financial Resilience, puts it bluntly:

“People treat insurance like a checkbox—not a strategy. They buy what’s easy, not what’s essential. The result? Catastrophic gaps when disaster strikes.”

The fix? Prioritize coverage based on risk, not marketing. Let’s break down the hierarchy.

The 7 Types of Insurance Ranked by Necessity

1. Health Insurance: The Non-Negotiable Foundation

Why it’s #1: Medical debt is the #1 cause of bankruptcy in the U.S. A single ER visit can cost $3,000+. Without coverage, one accident can wipe out decades of savings.

Actionable tip: If your employer offers a high-deductible plan, pair it with an HSA (Health Savings Account). It’s triple-tax-advantaged and builds a medical emergency fund.

2. Auto Insurance: Legal and Financial Armor

Why it’s #2: In 49 states, driving without auto insurance is illegal. But beyond legality, uninsured motorists cause 1 in 8 accidents (III, 2023). If you’re hit by one, you’re on the hook for repairs, medical bills, and lost wages.

Actionable tip: Always carry uninsured/underinsured motorist coverage. It’s cheap—often under $10/month—and could save you $50,000+.

3. Homeowners or Renters Insurance: Protecting Your Shelter

Why it’s #3: Your home is likely your biggest asset. A fire, burst pipe, or break-in can cost $10,000–$100,000 to fix. Renters? Your landlord’s policy doesn’t cover your stuff.

Actionable tip: Document everything. Take photos of your belongings and store them in the cloud. When disaster strikes, proof speeds up claims.

4. Disability Insurance: The Silent Lifesaver (Yes, Really)

Why it’s #4 (and why it shocks people): You’re three times more likely to become disabled before age 65 than to die (Council for Disability Awareness, 2024). Yet only 35% of workers have long-term disability coverage.

Actionable tip: If your employer offers it, take it. If not, get a private policy that covers 60–70% of your income. It’s cheaper than you think—often $20–$50/month.

5. Life Insurance: For Those Who Depend on You

Why it’s #5: If you have kids, a spouse, or co-signed debt, life insurance isn’t optional. A $500,000 term policy costs as little as $25/month for a healthy 30-year-old.

Actionable tip: Buy term life—not whole life. It’s 80% cheaper and does the job: replacing your income if you die.

6. Umbrella Insurance: The Overlooked Shield

Why it’s #6: Lawsuits are rising. If someone slips on your porch or your dog bites a neighbor, you could face a $1M+ judgment. Umbrella policies start at $150/year for $1M in coverage.

Actionable tip: Get umbrella insurance if you have assets over $500K or high-risk hobbies (e.g., boating, hosting parties).

7. Pet Insurance: Optional but Emotionally Critical

Why it’s #7: Vet bills average $1,500–$5,000 for emergencies. Pet insurance isn’t “necessary” for survival—but for many, it’s the difference between treatment and euthanasia.

Actionable tip: Enroll pets young. Pre-existing conditions are excluded, so early coverage locks in protection.

The Biggest Insurance Myth: “I’m Young and Healthy—I Don’t Need It”

This is the most dangerous lie in personal finance. 72% of uninsured adults under 35 say they’ll “get coverage later” (KFF, 2024). But “later” often means after a diagnosis, accident, or job loss—when premiums skyrocket or coverage is denied.

Dr. Simmons warns:

“Insurance isn’t about today. It’s about tomorrow’s ‘what ifs.’ The best time to buy is when you’re healthy, employed, and invisible to risk.”

Actionable tip: Review your coverage annually. Life changes—marriage, kids, new job—demand updated policies.

Insurance Coverage Comparison: What You Need vs. What You Think You Need

| Insurance Type | Necessity Level | Avg. Monthly Cost | Who Needs It? | Biggest Risk of Skipping |

|---|---|---|---|---|

| Health Insurance | Critical | $300–$600 | Everyone | Medical bankruptcy |

| Auto Insurance | Critical | $100–$250 | All drivers | Legal fines, financial ruin |

| Homeowners/Renters | High | $50–$150 | Homeowners, renters | Total loss of shelter/assets |

| Disability Insurance | High | $20–$50 | Income earners | Loss of income during illness |

| Life Insurance | Moderate | $25–$100 | Dependents, debtors | Family financial collapse |

| Umbrella Insurance | Moderate | $12–$25 | High-net-worth, high-risk | Lawsuit devastation |

| Pet Insurance | Low | $30–$60 | Pet owners | Euthanasia due to cost |

How to Build Your Insurance Safety Net in 30 Days

You don’t need to overhaul everything at once. Follow this 30-day plan:

- Week 1: Audit your current policies. What’s covered? What’s missing?

- Week 2: Get quotes for health, auto, and disability insurance. Compare at least three providers.

- Week 3: Add renters/homeowners and umbrella insurance if applicable.

- Week 4: Set up automatic payments and store digital copies in a secure cloud folder.

Actionable tip: Use a free tool like Policygenius or NerdWallet to compare rates. Don’t overpay for brand names.

FAQ

What is the most important type of insurance?

Health insurance is the most critical. Without it, a single medical emergency can lead to bankruptcy. It’s the foundation of all financial protection.

Do I need life insurance if I’m single?

Generally, no—unless you have co-signed debt (e.g., student loans) or aging parents who depend on you. Term life is cheap and can cover final expenses.

Is pet insurance worth it?

For many, yes—especially if you have a breed prone to illness (e.g., Bulldogs, German Shepherds). It prevents heartbreaking decisions due to cost.

How much disability insurance do I need?

Aim for 60–70% of your gross income. This covers essentials like rent, food, and utilities if you can’t work.

What’s the difference between whole and term life insurance?

Term life covers you for a set period (e.g., 20 years) and is far cheaper. Whole life is permanent but costs 5–10x more and includes a savings component most don’t need.

Final Thought: Protect Your Future, Not Just Your Present

Insurance isn’t about fear—it’s about freedom. Freedom to take risks, start businesses, raise families, and live boldly. The right coverage doesn’t just protect your wallet; it protects your peace of mind.

If this post helped you rethink your insurance strategy, share it with someone who’s one accident away from financial disaster. Tag a friend, parent, or coworker who needs to see this. Because the best time to prepare for the worst is before it happens.