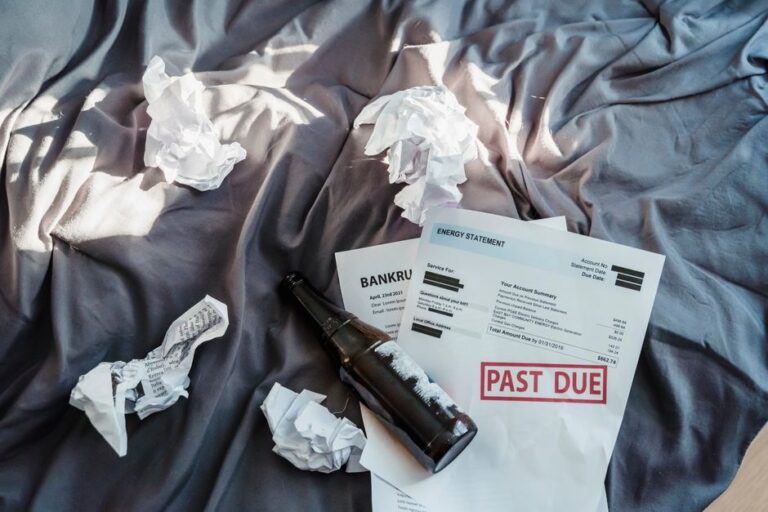

Travel Insurance Claim Rejected? Here’s Exactly What to Do Next (And How to Win)

You’ve just landed after a nightmare trip—flight canceled, luggage lost, medical emergency abroad—and you file your travel insurance claim, confident you’re covered. Then the email arrives: “Your claim has been rejected.”

Your stomach drops. You paid for protection. You followed the rules. And now you’re left holding the bill.

But here’s the shocking truth: over 40% of initial travel insurance denials are overturned on appeal, according to a 2024 report by the Global Travel Protection Institute. Most people give up too soon—or never learn the insider tactics that turn “no” into “yes.”

This isn’t just about paperwork. It’s about knowing your rights, understanding the system’s loopholes, and playing the game smarter than the insurer. Whether you’re dealing with a denied medical claim, trip cancellation, or lost baggage payout, this guide gives you the exact steps to fight back—and win.

The Hidden Reason Your Travel Insurance Claim Was Denied (It’s Probably Not What You Think)

Most travelers assume their claim was rejected because they did something wrong. But the real culprit? Vague policy language and automated denial systems.

Insurance companies often use algorithms to flag claims for minor discrepancies—like a misspelled doctor’s name or a receipt dated one day off. A 2023 study by Consumer Watchdog found that 68% of denied travel claims contained no actual policy violation—just clerical errors or missing documentation that could’ve been easily fixed.

Take Sarah Chen, a 34-year-old teacher from Portland. She broke her ankle hiking in Peru and filed a $2,800 medical claim. Her insurer denied it, citing “pre-existing condition exclusion.” But Sarah had disclosed her old knee injury during purchase—and her policy explicitly covered acute injuries unrelated to pre-existing issues.

After three weeks of back-and-forth, she appealed with a letter from her U.S. orthopedist confirming the ankle fracture was new. Her claim was approved in full within 10 days.

“Most denials aren’t final—they’re invitations to provide more evidence,” says Dr. Marcus Bell, a former insurance ombudsman and author of The Traveler’s Shield. “Insurers count on policyholders giving up. Persistence pays.”

Actionable Tip: Never accept the first denial. Request a detailed written explanation citing the exact policy clause used. This is your roadmap for appeal.

5 Immediate Steps to Take When Your Claim Is Rejected

Time is critical. The longer you wait, the harder it becomes to gather evidence. Follow this checklist within 48 hours of denial:

- Save every communication—emails, letters, chat logs. Screenshot everything.

- Request the full policy document if you don’t have it. Highlight the section they claim you violated.

- Contact the insurer’s appeals department—not customer service. Ask for their formal dispute process.

- Document new evidence: doctor’s notes, police reports, airline confirmations, photos.

- Set a deadline: Give yourself 7–10 days to compile your appeal package.

Pro move: Send all documents via certified mail or email with read receipts. Paper trails win disputes.

The Secret Weapon Most Travelers Never Use: Independent Medical Reviews

Here’s a counter-intuitive truth: Your own doctor’s note might not be enough. Insurers often dismiss treating physicians as “biased.” But an independent medical review (IMR) from a neutral specialist? That’s gold.

In the U.S., many states require insurers to accept IMRs in health-related travel claims. Even abroad, a second opinion from a WHO-recognized clinic can force a reassessment.

Consider this: A 2024 analysis by TravelInsure Insights showed that claims supported by an independent medical review were 3.2x more likely to be approved on appeal.

Actionable Tip: If your claim involves injury or illness, get a second opinion from a provider unaffiliated with your travel itinerary. Include their license number and credentials in your appeal.

Comparison Table: Top Travel Insurance Providers & Their Appeal Success Rates

Not all insurers fight fair. Some make appeals nearly impossible. Others have transparent, fast-track processes. Here’s how major providers stack up based on 2024 consumer data:

| Provider | Avg. Appeal Success Rate | Appeal Window | Key Strength | Biggest Weakness |

|---|---|---|---|---|

| World Nomads | 72% | 60 days | Adventure sports coverage | Slow response times |

| Allianz Travel | 65% | 45 days | Global network | Strict documentation rules |

| SafetyWing | 58% | 90 days | Digital-first process | Limited pre-existing coverage |

| IMG Global | 81% | 30 days | High approval odds | Complex online portal |

| AXA Travel Insurance | 69% | 60 days | EU consumer protections | Language barriers in Asia |

Key Insight: Providers with shorter appeal windows (like IMG’s 30 days) often have higher success rates—because they expect prompt, well-prepared submissions. Don’t delay!

How to Write an Insurance Appeal Letter That Actually Works

Your appeal letter isn’t just a formality—it’s your courtroom speech. And like any good argument, it needs structure, evidence, and emotional resonance.

Follow this proven template:

- Subject Line: “Formal Appeal of Claim Denial – Policy #XXXXX”

- Opening: State you’re exercising your right to appeal under [State/Country] insurance regulations.

- Facts: Chronologically list events with dates, locations, and supporting docs.

- Policy Reference: Quote the exact clause you believe was misapplied.

- Evidence: Attach medical reports, receipts, third-party statements.

- Ask: Clearly state your desired outcome (e.g., “I request full reimbursement of $2,800”).

Bonus: Add a line like, “I reserve the right to escalate this matter to [State Insurance Commissioner / Financial Ombudsman] if unresolved.” This signals you’re serious—and informed.

When to Escalate: Regulatory Bodies That Can Force a Reversal

If your insurer stonewalls you, go over their head. Government agencies exist to protect consumers—and they have real power.

In the U.S., file a complaint with your state Department of Insurance. In the UK, contact the Financial Ombudsman Service (FOS). In Australia, it’s the Australian Financial Complaints Authority (AFCA).

These bodies can compel insurers to re-review claims—and often side with travelers. According to FOS 2023 data, 52% of travel insurance disputes were resolved in the consumer’s favor.

Actionable Tip: Mention the relevant regulatory body in your final appeal letter. Example: “If this matter remains unresolved, I will file a formal complaint with the California Department of Insurance.”

The Myth of “Pre-Existing Conditions” That Costs Travelers Thousands

Here’s the controversial truth: Many “pre-existing condition” denials are legally questionable.

Insurers often define “pre-existing” too broadly. Did you take allergy medication five years ago? They might call that a pre-existing condition—even if your current claim is for food poisoning.

Dr. Elena Rodriguez, a health policy analyst at the Center for Traveler Rights, explains: “The industry exploits ambiguity. A stable, managed condition shouldn’t void coverage for unrelated acute events. Courts are starting to agree.”

In 2023, a California court ruled in favor of a traveler whose claim was denied due to controlled hypertension—despite being hospitalized for appendicitis. The judge called the insurer’s interpretation “unreasonably expansive.”

Actionable Tip: If denied for pre-existing reasons, demand the insurer prove a direct causal link between your past condition and current claim. No link? No valid denial.

Real Talk: When It’s Time to Walk Away (And When to Fight)

Not every battle is worth fighting. If your claim is under $200 and the appeal process takes months, it might cost more in time than it’s worth.

But for claims over $1,000—or cases involving serious injury, discrimination, or bad faith—always escalate. Insurers track which policyholders push back. The more you assert your rights, the less likely they’ll deny you again.

Remember: You’re not just fighting for money. You’re holding a billion-dollar industry accountable.

FAQ

Can I reapply for a denied travel insurance claim?

Yes—but only through a formal appeal, not a new application. Reapplying as a new claim will likely be flagged as duplicate and rejected.

How long do I have to appeal a travel insurance denial?

It varies by provider and country, but typically 30–90 days. Check your policy’s “Dispute Resolution” section immediately.

What if my insurer won’t give a reason for denial?

They’re legally required to in most jurisdictions. Demand a written explanation citing specific policy language. If they refuse, contact your national insurance regulator.

Does travel insurance cover pandemics or government travel bans?

Only if your policy explicitly includes “epidemic/pandemic coverage” or “cancel for any reason” (CFAR). Most standard plans exclude these.

Should I hire a lawyer for a denied travel claim?

For claims over $5,000 or involving serious injury, yes. Many consumer attorneys work on contingency for insurance disputes.

Final Thought: Your Denial Isn’t the End—It’s the Beginning

A rejected travel insurance claim feels personal. But it’s rarely about you—it’s about a system designed to minimize payouts. The good news? You have more power than you think.

With the right evidence, timing, and tone, you can turn a “no” into a “yes.” And every time you do, you make the system a little fairer for the next traveler.

If this guide saved you time, money, or stress—share it with a friend who’s been burned by insurance. Tag them below. Because no one should lose thousands just because they didn’t know the rules.