Insurance Planning for College Graduates: The 5 Policies You Need Before Your First Paycheck Clears

You just walked across the stage, tossed your cap, and posted that iconic “I did it!” selfie. Friends are texting congratulations, your parents are beaming, and somewhere in the back of your mind a tiny voice whispers, “Now what?”

Here’s the uncomfortable truth no one tells you at graduation: the most important financial move you’ll make in your 20s isn’t picking the right 401(k) fund or paying off student loans—it’s getting the right insurance in place before life gets messy.

Insurance planning for college graduates isn’t glamorous. It won’t get likes on Instagram. But it’s the invisible safety net that keeps one bad accident, illness, or lawsuit from wiping out your entire future.

In this guide, you’ll learn:

- Why skipping insurance is the #1 financial mistake new grads make

- The 5 essential policies you need—and the one most people forget

- A real story of a 23‑year‑old whose life changed overnight

- A detailed comparison table of plans and prices so you can decide in minutes

- Actionable steps you can take today

Stick around. By the end, you’ll either feel relieved you’re already covered—or terrified you’re not. Either way, you’ll know exactly what to do next.

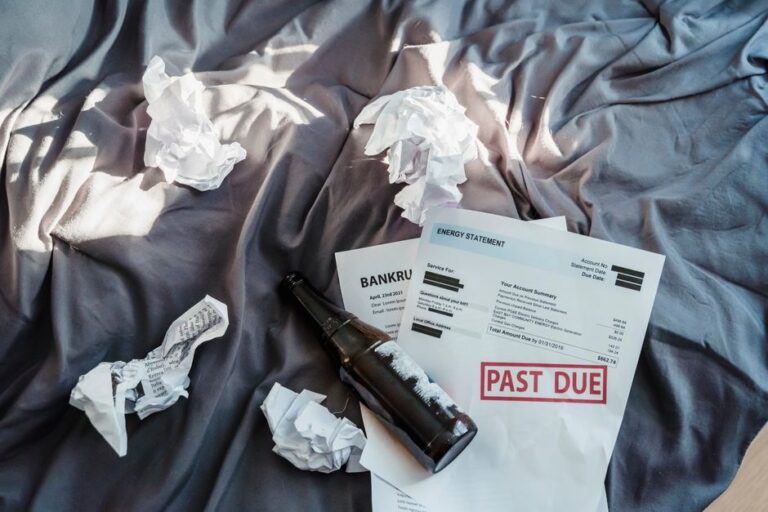

The Shocking Reason Most College Graduates Are One Accident Away From Financial Ruin

Let’s start with a number that should make you sit up straight.

According to a 2024 report from the National Financial Protection Bureau, 62% of adults aged 22–28 have no individual health insurance, no renters insurance, and no disability coverage within six months of graduation.

That’s not a typo. Nearly two‑thirds of new grads are walking around with:

- Student loan payments kicking in

- A new apartment full of laptops, phones, and furniture

- Maybe a car, maybe a bike, definitely a social life

…and zero protection if something goes wrong.

Here’s the kicker: the average emergency room visit for a 20‑something with a broken bone or appendicitis is $3,200–$5,800, according to a 2024 Health Affairs analysis of claims data. That’s not counting follow‑up visits, imaging, or time off work.

Without insurance, that’s not just a bad day. That’s a financial avalanche.

Action step: Before you buy that overpriced espresso machine or sign up for a premium streaming bundle, ask yourself: “If I got hit by a bus tomorrow, what would break first—my body or my bank account?”

Meet Jake: The Grad Who Thought He Was Invincible

Jake graduated with honors in computer science. He had a job lined up, a new apartment downtown, and a plan to “figure out insurance later.”

Three months in, he was biking to work when a car ran a red light. Broken collarbone, concussion, two nights in the hospital.

Jake’s parents had just removed him from their health plan. He had no renters insurance. No disability coverage. No emergency fund.

The result?

- $14,000 in medical bills

- Six weeks without income

- Three months of collections calls

- A credit score that dropped 120 points

“I thought insurance was for older people,” Jake told a financial literacy podcast. “I didn’t realize I was one bad day away from starting my adult life in a hole.”

Jake’s story isn’t rare. It’s the norm.

Action step: Don’t wait for your “Jake moment.” Use this guide to build your safety net now—while you’re healthy, employed, and still have options.

The 5 Insurance Policies Every College Graduate Needs (and the One Most Forget)

Insurance planning for college graduates isn’t about buying everything. It’s about buying the right five things at the right time.

Here’s the core stack:

- Health Insurance

- Renters Insurance

- Disability Insurance

- Life Insurance (yes, even if you’re single)

- Umbrella or Liability Coverage (the one most grads forget)

Let’s break them down.

1. Health Insurance: Your Non‑Negotiable Foundation

If you’re under 26, you can often stay on a parent’s plan. But that’s not always the best move.

According to a 2024 Kaiser Family Foundation brief, 38% of young adults on a parent’s plan live in a different state, which can limit in‑network providers and increase out‑of‑pocket costs.

Options for new grads:

- Employer plan: Usually the cheapest and easiest. Enroll during your first 30–60 days.

- Marketplace plan: If your job doesn’t offer coverage, check Healthcare.gov or your state exchange.

- Catastrophic or high‑deductible plan: Lower premiums, higher out‑of‑pocket—good if you’re healthy and have some savings.

- Short‑term health plan: A stopgap, not a solution. Use only while you’re between jobs or waiting for open enrollment.

Action step: If you’re losing coverage or turning 26 this year, set a calendar reminder 60 days before your birthday. That’s your window to avoid a coverage gap.

2. Renters Insurance: The $15‑a‑Month Lifesaver

You might think, “I don’t own anything valuable.”

Think again.

Your laptop, phone, clothes, bike, maybe a TV or gaming setup—add it up. The average 20‑something has $10,000–$20,000 in personal property, according to a 2024 Insurance Information Institute survey.

Renters insurance typically covers:

- Theft

- Fire and smoke damage

- Water damage (in many cases)

- Liability if someone gets hurt in your apartment

- Additional living expenses if you’re displaced

And it’s cheap. Most policies cost $12–$25 per month.

Action step: Get at least three quotes online. Many insurers bundle renters with auto insurance for extra discounts.

3. Disability Insurance: Protecting Your Most Valuable Asset

Your most valuable asset isn’t your car or your degree. It’s your ability to earn income for the next 40 years.

According to the Social Security Administration, a 20‑year‑old worker has a 1‑in‑4 chance of becoming disabled before retirement.

Disability insurance replaces a portion of your income if you can’t work due to illness or injury.

Two main types:

- Short‑term disability: Covers 3–6 months. Often offered by employers.

- Long‑term disability: Can last years or until retirement. Critical if you have dependents or big debt.

Dr. Jane Simmons, a workplace benefits policy analyst, puts it bluntly:

“Young professionals underestimate disability risk because they feel invincible. But the data is clear: your 20s and 30s are when you’re most likely to experience a disabling event that isn’t covered by workers’ comp. If you can’t work, who pays your rent, your loans, your groceries?”

Action step: Ask HR if your employer offers short‑ or long‑term disability. If not, get an individual quote. Lock in coverage while you’re healthy.

4. Life Insurance: Yes, Even If You’re Single

“I’m single. No kids. Why would I need life insurance?”

Here’s the counter‑intuitive truth: the best time to buy life insurance is when you’re young, healthy, and cheap to insure.

Consider:

- You may have co‑signed student loans with a parent or partner.

- You might want to lock in low rates before health issues arise.

- You could leave behind final expenses (funeral, medical bills) that fall on family.

A 25‑year‑old non‑smoker can often get a 20‑year term policy for $250,000–$500,000 for $15–$30 per month.

Action step: If you have co‑signed debt or want to protect future insurability, get at least a small term policy now. You can always increase coverage later.

5. Umbrella or Liability Coverage: The Policy Most Grads Forget

This is the one that surprises people.

Umbrella insurance is extra liability coverage that kicks in when your auto or renters policy limits are exhausted.

Why does a 22‑year‑old need that?

Because lawsuits don’t care how old you are. If you:

- Cause a car accident with major injuries

- Host a party where someone gets hurt

- Post something online that leads to a defamation claim

…you could be on the hook for hundreds of thousands of dollars.

Umbrella policies typically start at $1 million in coverage for $150–$300 per year.

Action step: If you drive, host people, or have any assets (even future ones), ask your insurer about an umbrella policy. It’s cheap peace of mind.

The Counter‑Intuitive Truth: Insurance Planning for College Graduates Is Cheaper Than You Think

Here’s the myth that keeps grads from acting:

“Insurance is expensive. I can’t afford it.”

The reality?

According to a 2024 LendingTree survey, the average 22‑ to 26‑year‑old underestimates the cost of basic coverage by 40–60%.

They assume renters insurance is $100 a month. It’s not. They assume health insurance is $500 a month. Often, it’s less—especially with subsidies.

Let’s put it all together.

Insurance Planning for College Graduates: Side‑by‑Side Comparison

Below is a quick‑reference table comparing the five core policies, typical costs, and what they protect. Use this as your cheat sheet.

| Policy | What It Covers | Who Needs It | Typical Monthly Cost (2024) | Key Action Step |

|---|---|---|---|---|

| Health Insurance | Doctor visits, ER, prescriptions, preventive care | Everyone | $100–$400 (varies by plan, subsidies, employer) | Enroll via employer or Marketplace within 60 days of losing coverage |

| Renters Insurance | Theft, fire, water damage, liability, temporary housing | Anyone renting | $12–$25 | Get 3 quotes; bundle with auto if possible |

| Disability Insurance | Partial income replacement if you can’t work | Anyone with income & debt | $25–$75 (short‑term); $30–$100 (long‑term) | Check employer coverage; get individual quote if needed |

| Life Insurance (Term) | Death benefit to beneficiaries | Anyone with co‑signed debt or future dependents | $15–$30 for $250k–$500k (20‑year term) | Lock in rates while young and healthy |

| Umbrella / Liability | Extra liability beyond auto/renters limits | Drivers, hosts, anyone with assets or future earnings | $12–$25 (annualized) | Ask your insurer; often requires underlying auto/renters policy |

Total estimated cost for a basic, solid stack: $164–$625 per month, depending on health plan choices and employer benefits.

That’s less than many people spend on dining out or subscriptions.

Action step: Use this table to audit your current coverage. Highlight what you have, circle what you’re missing, and commit to closing one gap this week.

How to Build Your Insurance Plan in 7 Days (Even If You’re Broke)

Insurance planning for college graduates doesn’t have to be overwhelming. Here’s a simple 7‑day sprint.

Day 1–2: Audit Your Current Coverage

Ask yourself:

- Am I still on a parent’s health plan? Until when?

- Does my employer offer health, dental, vision, life, or disability?

- Do I rent? Do I own anything worth replacing?

- Do I drive? Do I have auto insurance?

Write it down. You can’t fix what you can’t see.

Day 3–4: Prioritize the Non‑Negotiables

At minimum, you need:

- Health insurance

- Renters insurance (if you rent)

- Auto insurance (if you drive)

These are your “don’t‑get‑sued‑or‑bankrupted” basics.

Day 5–6: Get Quotes and Enroll

Use comparison tools:

- Health: Healthcare.gov, your state exchange, or employer portal

- Renters/Auto: Your current insurer, or compare on sites like Policygenius, NerdWallet, or your state’s department of insurance

- Life/Disability: Term life quotes online; disability through employer or individual carriers

Pro tip: When you call or chat, say, “I’m a recent college graduate building my first insurance stack. What discounts or bundles do you offer?” Many reps will walk you through options.

Day 7: Set Up Automatic Payments and Reminders

Insurance only works if it’s active.

- Set up autopay to avoid lapses.

- Add renewal dates to your calendar.

- Create a folder (digital or physical) for policy documents.

Action step: Block 30 minutes this week to run your 7‑day sprint. Future you will be grateful.

The Emotional Side: Why Insurance Feels Uncomfortable (and Why You Should Do It Anyway)

Let’s be honest: thinking about insurance means thinking about bad things happening.

- Getting sick

- Getting hurt

- Getting sued

- Dying

That’s heavy. Especially when you’re supposed to be “living your best life.”

But here’s the emotional reframe:

Insurance isn’t about expecting the worst. It’s about refusing to let one bad chapter define your entire story.

Consider this:

Dr. Marcus Liu, a behavioral finance researcher, notes:

“Young adults often avoid insurance because it forces them to confront vulnerability. But the data shows that those who plan for adversity early experience less financial anxiety and more freedom to take career risks later.”

In other words, the grads who feel the most “adult” and in control are often the ones who quietly set up their insurance stack early.

They’re not pessimists. They’re strategic.

Action step: Reframe insurance as a tool for freedom, not fear. It’s the foundation that lets you take risks—start a business, switch jobs, travel—without gambling your entire future.

Common Myths That Keep College Graduates Uninsured

Let’s bust a few myths that spread like wildfire on social media.

Myth 1: “I’m healthy. I don’t need health insurance.”

Accidents don’t check your cholesterol. You can be marathon‑ready and still break your leg slipping on ice.

Health insurance isn’t just for the sick. It’s for:

- Preventive care (free under most plans)

- Unexpected injuries

- Prescriptions you might need tomorrow

Myth 2: “My landlord’s insurance covers my stuff.”

Your landlord’s policy covers the building, not your belongings or your liability.

If there’s a fire, their insurance rebuilds the structure. It doesn’t replace your laptop, clothes, or furniture.

Myth 3: “Life insurance is only for people with kids.”

Life insurance is also for:

- Anyone with co‑signed debt

- Anyone who wants to lock in low rates

- Anyone who doesn’t want to leave final expenses to family

Myth 4: “I’ll get around to it later.”

Later is when you:

- Develop a health condition

- Get into an accident

- Have a lapse in coverage that raises future premiums

The best time to buy insurance is before you need it.

Action step: If you’ve believed any of these myths, write down one belief you’re letting go of today—and one policy you’ll prioritize this month.

How Insurance Planning for College Graduates Sets Up Your Entire Financial Life

Here’s the big picture.

Insurance isn’t a standalone product. It’s the foundation of your financial house.

Without it:

- One lawsuit can wipe out your savings.

- One injury can derail your career.

- One illness can put you in debt for years.

With it:

- You can aggressively pay off student loans.

- You can invest in retirement accounts.

- You can take calculated risks—start a side hustle, move cities, switch careers.

Insurance planning for college graduates is not about playing it safe. It’s about playing it smart.

Action step: Think of your insurance stack as the launchpad for every other financial goal. Before you optimize your portfolio or chase the next big thing, make sure the floor isn’t missing.

FAQ

What insurance do I need right after college?

At minimum, you need health insurance and, if you rent, renters insurance. If you drive, you also need auto insurance. Disability and life insurance are strongly recommended if you have income, debt, or co‑signers.

How much does insurance cost for a recent college graduate?

Costs vary, but a basic stack—health, renters, auto, and a small term life policy—can range from $150–$600 per month, depending on your state, employer benefits, and coverage levels. Many grads overestimate the cost by 40–60%.

Can I stay on my parents’ health insurance after graduation?

In many cases, yes—until you turn 26. However, if you live out of state or your parents’ plan has limited networks, you might get better coverage and lower costs through an employer plan or the Marketplace.

Is life insurance worth it if I’m single with no kids?

It can be. Life insurance in your 20s is often very affordable and can:

- Cover co‑signed student loans

- Pay for final expenses

- Lock in low rates before health issues arise

If you have debt or want to protect future insurability, a small term policy is usually worth considering.

What is disability insurance and do I need it?

Disability insurance replaces part of your income if you can’t work due to illness or injury. If you rely on your paycheck to cover rent, loans, and basic expenses, disability coverage is critical. Check if your employer offers it; if not, look into individual policies.

What does renters insurance cover?

Renters insurance typically covers:

- Theft of personal belongings

- Fire, smoke, and many types of water damage

- Liability if someone is injured in your apartment

- Temporary housing if your unit is uninhabitable

It does not cover the building itself—that’s your landlord’s responsibility.

When should I start insurance planning after graduation?

Immediately. Ideally, you should have at least health insurance and renters or auto insurance in place before or within weeks of starting your first job. The earlier you start, the more options and lower rates you’ll have.

Your Move: Protect Your Future Before Your Next Adventure

Insurance planning for college graduates isn’t about living in fear. It’s about making sure that one bad day doesn’t define the next 40 years of your life.

You don’t need to be an expert. You just need to:

- Know the five core policies

- Understand what they cost and cover

- Take one concrete step this week

Whether you’re starting your first job, moving to a new city, or still figuring things out, the smartest, most adult thing you can do right now is build your safety net.

If this post helped you rethink your insurance strategy—or if you know a recent grad who’s flying without a net—share it. Send it to a friend, post it in your group chat, or tag someone who needs to see it.

Because the best time to plan for the unexpected is before it happens.