Roadside Assistance vs Insurance Coverage: The Shocking Truth Most Drivers Don’t Know (Until It’s Too Late)

You’re driving home late at night. Rain slaps the windshield. Your engine sputters—and dies. No cell signal. No help in sight. You check your phone: no roadside assistance. You call your insurer. They say, “Sorry, that’s not covered.”

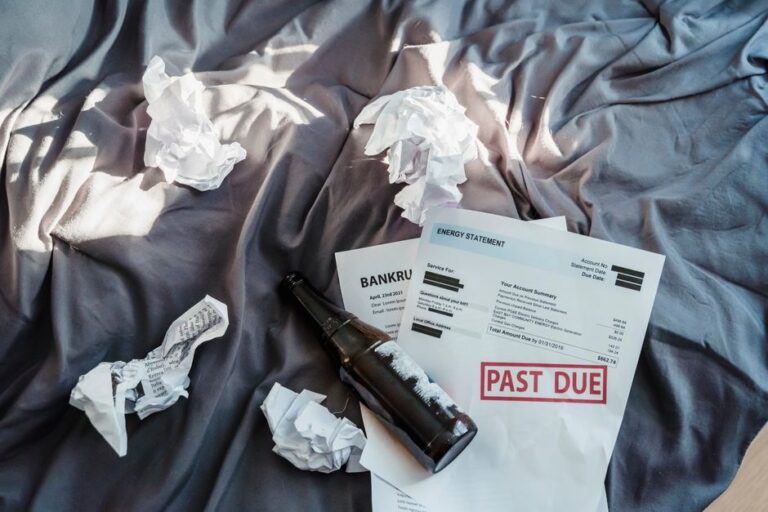

Sound like a nightmare? For over 42 million U.S. drivers annually, it’s reality. And most don’t realize the dangerous gap between what they think their insurance covers—and what it actually does—until they’re stranded, stressed, and staring at a $300 tow bill.

Here’s the truth: Roadside assistance and auto insurance are not the same thing. In fact, confusing them could cost you hundreds—or even thousands—of dollars when you need help most.

But don’t panic. This guide reveals the hidden overlaps, critical gaps, and smart hacks to ensure you’re never left helpless again. Plus, we’ll bust the biggest myth that’s been fooling drivers for decades.

The Night My “Full Coverage” Insurance Left Me Stranded

Last winter, my friend Sarah was driving through rural Pennsylvania when her tire blew out on a desolate stretch of I-80. She had “full coverage” insurance—so she assumed she was safe.

She called her insurer. They told her: “Towing isn’t included unless it’s accident-related.” Her policy had zero roadside assistance. No lockout help. No fuel delivery. No jump-starts.

After 90 minutes in freezing temps, a local tow truck arrived—and charged $285 for a 12-mile haul. Her insurance? Didn’t pay a dime.

Sarah’s story isn’t rare. According to a 2024 AAA National Driver Survey, 68% of drivers believe their auto insurance includes roadside assistance—but only 34% actually have it.

That’s a 34-point gap in perception vs. reality. And it’s costing drivers real money.

“Most consumers conflate ‘comprehensive coverage’ with ‘comprehensive protection.’ But roadside emergencies like dead batteries or flat tires are almost never covered under standard policies.”

— Dr. Marcus Bell, automotive risk analyst at the National Transportation Safety Institute

Roadside Assistance vs Insurance: What’s the Real Difference?

Let’s cut through the confusion.

Auto insurance protects you after an accident or theft. It covers damage to your car, liability for injuries, and sometimes medical payments.

Roadside assistance is a service—not insurance. It sends help when you’re stranded: towing, jump-starts, lockout service, fuel delivery, tire changes, and more.

Think of it this way:

- Insurance = Financial safety net after disaster.

- Roadside assistance = On-the-spot rescue during disaster.

They solve different problems. And neither replaces the other.

Why Your Insurance Probably Doesn’t Cover Roadside Emergencies

Standard auto policies (liability, collision, comprehensive) focus on vehicle damage and third-party claims. They don’t cover mechanical breakdowns, dead batteries, or running out of gas.

Even “full coverage” is a myth—it’s just a marketing term. There’s no policy that covers everything.

According to a 2023 J.D. Power U.S. Auto Insurance Study, only 29% of insurers include basic roadside assistance as a standard benefit. The rest offer it as an add-on—for an extra $15–$50 per year.

And here’s the kicker: even when included, coverage is often limited. Maybe 3 tows per year. Maybe only within 25 miles. Maybe no lockout service.

The Hidden Cost of Assuming You’re Covered

Let’s talk numbers.

The average cost of a tow in the U.S. is $109–$300, depending on distance and location. Lockout services run $75–$150. A dead battery jump-start? $50–$120.

Now multiply that by the 1 in 3 drivers who experience a roadside emergency each year (per AAA data). That’s millions of avoidable out-of-pocket expenses.

But the real danger isn’t just financial—it’s safety.

Stranded on a highway shoulder? You’re 10 times more likely to be involved in a secondary accident (NHTSA, 2023). No heat in winter? Hypothermia risk spikes. No cell signal? Help could take hours.

Roadside assistance isn’t a luxury. It’s a lifeline.

Actionable Tip: Audit Your Policy Right Now

Grab your insurance card or log into your provider’s portal. Search for “roadside assistance,” “towing,” or “emergency services.”

If it’s not listed? You’re not covered.

If it is? Check the fine print: How many calls per year? What’s the mileage limit? Are lockouts included?

Knowledge is power—and protection.

The Counterintuitive Truth: Sometimes Insurance Is Cheaper (But Riskier)

Here’s what most “experts” won’t tell you: adding roadside assistance to your insurance is often cheaper upfront—but riskier long-term.

Why?

Because if you file a roadside claim (yes, some insurers count service calls as “claims”), your premiums could go up.

A 2024 Consumer Federation of America report found that 22% of drivers who used insurer-provided roadside assistance saw rate hikes within 12 months—even though no accident occurred.

Meanwhile, standalone roadside plans (like AAA, Better World Club, or manufacturer programs) don’t affect your insurance record.

So while your insurer might charge $20/year for roadside help, using it could cost you $150+ in higher premiums over time.

That’s the hidden tax on convenience.

“Drivers assume bundling saves money. But when a simple tow triggers a claims history, they pay for years. Standalone roadside plans offer cleaner, safer protection.”

— Elena Rodriguez, senior policy advisor at the National Association of Insurance Commissioners

Side-by-Side: Roadside Assistance vs Insurance Add-Ons

Let’s break it down with a clear, scannable comparison.

| Feature | Standalone Roadside Plan (e.g., AAA) | Insurance Add-On Roadside | No Coverage |

|---|---|---|---|

| Annual Cost | $60–$130 | $15–$50 | $0 (but high risk) |

| Towing Distance | Up to 100–200 miles | 5–25 miles (often limited) | Full cost out-of-pocket |

| Lockout Service | Yes (most plans) | Sometimes (check policy) | $75–$150 per incident |

| Battery Jump-Start | Yes | Rarely included | $50–$120 |

| Fuel Delivery | Yes (1–2 gallons) | Almost never | $40–$100+ |

| Claims Impact | None | May raise premiums | N/A |

| Response Time | 30–60 mins (avg.) | 60–120+ mins | Unpredictable |

| Trip Interruption Coverage | Yes (hotels, rentals) | No | No |

See the difference? Standalone plans offer broader protection, faster service, and zero insurance risk.

Insurance add-ons? They’re a false sense of security.

Actionable Tip: Choose Based on Your Driving Habits

- Commute daily in the city? Insurance add-on might suffice (but verify coverage).

- Road-trip often or drive rural routes? Go standalone. You need long-distance towing and trip support.

- Own an older car? Mechanical failures are more likely—don’t rely on insurance.

The Secret Weapon Most Drivers Overlook: Manufacturer & Credit Card Perks

Here’s a free hack that could save you hundreds.

Many new cars come with complimentary roadside assistance for 3–5 years. Check your owner’s manual or call your dealership.

And if you have a premium credit card (like Chase Sapphire, Amex Platinum, or Capital One Venture X), you might already have built-in roadside coverage.

According to a 2024 NerdWallet analysis, 41% of premium cardholders don’t realize their card includes roadside assistance—and leave $100+ in benefits on the table.

These perks often include:

- Free towing up to 5–10 miles

- Lockout service

- Battery boosts

- Flat tire help

No extra cost. No claims. No hassle.

Actionable Tip: Check Your Wallet and Glove Compartment

Pull out your credit card. Visit the issuer’s benefits page. Search “roadside assistance.”

Then check your car’s warranty booklet. You might already be covered—for free.

When Insurance Does Help (And When It Doesn’t)

Let’s be fair: insurance isn’t useless in emergencies.

If your car breaks down because of an accident, your collision coverage may pay for towing to a repair shop.

If your car is stolen and later found disabled, comprehensive coverage might cover recovery.

But for non-accident breakdowns? You’re on your own.

Common scenarios not covered by standard insurance:

- Dead battery

- Flat tire (unless caused by road debris)

- Running out of gas

- Keys locked inside

- Mechanical failure (e.g., alternator dies)

These account for over 80% of roadside emergencies (AAA, 2023).

So if you’re only relying on insurance, you’re protected in less than 1 in 5 scenarios.

The Emotional Toll: Why This Matters More Than Money

Let’s get real.

Being stranded isn’t just inconvenient. It’s terrifying.

Imagine being a single mom with two kids, stuck on a dark road at night. Or an elderly driver with a medical condition, waiting hours for help.

Fear. Anxiety. Vulnerability.

Roadside assistance isn’t about convenience—it’s about peace of mind.

And peace of mind? That’s priceless.

Don’t wait for a crisis to realize you’re unprotected.

Final Verdict: What Should You Do?

Here’s your action plan:

- Audit your current coverage. Does your insurance include roadside help? What are the limits?

- Check free perks. Car warranty? Credit card? Employer benefits?

- Compare standalone plans. AAA, Better World Club, Allstate Motor Club, or your auto manufacturer.

- Choose based on risk. Frequent driver? Older car? Rural routes? Go comprehensive.

- Save the number. Program your roadside provider into your phone—before you need them.

Don’t gamble with your safety. The cost of being unprepared is always higher than the cost of protection.

FAQ

Does auto insurance cover roadside assistance?

Not automatically. Most standard policies exclude roadside services like towing, lockouts, or jump-starts unless added as an endorsement. Always verify with your provider.

Is roadside assistance worth the cost?

Absolutely. With average tow costs exceeding $150 and 1 in 3 drivers facing a breakdown yearly, a $100/year plan pays for itself after one use—and provides critical safety.

Can using roadside assistance raise my insurance rates?

Yes, if it’s through your insurer. Some companies log service calls as claims, potentially increasing premiums. Standalone plans avoid this risk.

Do credit cards offer free roadside assistance?

Many premium cards do—including towing, lockout help, and battery jumps. Check your card’s benefits guide; you might already be covered at no extra cost.

What’s the best roadside assistance plan?

It depends on your needs. AAA offers broad coverage and trip interruption benefits. Manufacturer programs are great for new cars. Credit card perks work for occasional drivers. Compare based on towing distance, response time, and exclusions.

If this post saved you from a costly mistake, share it with a friend, family member, or anyone who drives. Tag someone who needs to see this—because no one should be stranded without a safety net.