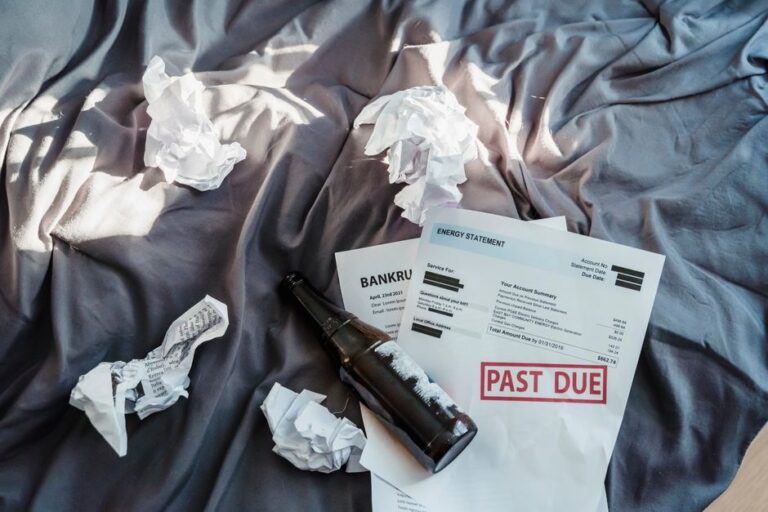

Why Health Insurance Denies Claims — And How to Fight Back and Win

You open the envelope and your stomach drops. “Claim Denied.” Not approved. Not partially covered. Flat-out rejected. You did everything right — you went to an in-network doctor, you paid your premiums on time, and you assumed you were protected. But somehow, the insurance company said no.

If this has happened to you, you’re not alone. According to a 2024 Health Affairs study, approximately 17% of in-network health insurance claims are denied annually — that’s roughly 1 in 6 claims that patients and doctors file. And here’s the part that should make you furious: only about 0.2% of patients ever appeal those denials. Insurance companies are banking on your silence.

But here’s the counterintuitive truth that the insurance industry doesn’t want you to know: when patients do appeal, they win roughly 73% of the time. That means the denial isn’t the end of the story — it’s just the opening move in a game you can absolutely win if you know the rules.

This guide is your playbook. We’ll break down exactly why claims get denied, reveal the real reasons behind those cryptic rejection letters, and give you a step-by-step battle plan to fight back. Whether you just got your first denial or you’re drowning in a stack of them, this article will change how you think about your insurance company forever.

The Real Reasons Your Health Insurance Denies Claims (It’s Not What You Think)

Most people assume their claim was denied because the treatment wasn’t medically necessary or because they made a mistake. While those are real reasons, the full picture is far more complex — and far more infuriating.

Here are the most common reasons health insurance companies deny claims, ranked by frequency:

1. “Lack of Medical Necessity” — The Catch-All Excuse

This is the number one reason insurers deny claims, accounting for roughly 32% of all denials. The insurance company essentially argues that the procedure, test, or treatment wasn’t necessary — even when your doctor ordered it. The problem? The definition of “medical necessity” is often written by the insurance company itself, not by medical professionals.

What you can do now: Ask your doctor to write a detailed letter of medical necessity that specifically references the clinical guidelines your insurer uses. Match their language with their own rules.

2. Coding Errors and Administrative Mistakes

Believe it or not, a significant portion of denials — estimated at 15-20% — are caused by simple clerical errors. A wrong diagnostic code, a typo in your date of birth, or a mismatched procedure code can trigger an automatic denial. These aren’t judgment calls about your health. They’re bureaucratic failures.

What you can do now: Always request an itemized bill and an Explanation of Benefits (EOB). Compare the codes on both. If something doesn’t match your actual visit, call your provider’s billing department and ask them to correct and resubmit.

3. Pre-Authorization and Referral Requirements

Many plans require pre-approval before certain procedures or specialist visits. If your doctor’s office didn’t get that pre-authorization — or if the authorization expired — the claim gets denied. This is one of the most frustrating denial types because it often isn’t the patient’s fault at all.

What you can do now: Before any non-emergency procedure, call your insurance company and ask: “Is pre-authorization required for this specific CPT code?” Get the authorization number in writing.

4. Out-of-Network Provider Issues

You went to an in-network hospital, but the anesthesiologist who treated you wasn’t in your network. According to a 2023 Kaiser Family Foundation report, about 18% of emergency room visits involve at least one out-of-network provider, often without the patient’s knowledge. This is known as a “surprise bill” scenario, and while the No Surprises Act has helped, loopholes still exist.

What you can do now: For every visit, ask every provider — including radiologists, pathologists, and anesthesiologists — whether they’re in your network. Document the answer.

5. The “Experimental or Investigational” Label

Insurance companies sometimes deny cutting-edge treatments by labeling them experimental, even when they’ve been FDA-approved and are standard practice. This is especially common with newer cancer treatments, mental health therapies, and rare disease medications.

What you can do now: Gather peer-reviewed studies supporting the treatment and submit them with your appeal. Clinical evidence is your strongest weapon here.

“Insurance denials are often not about whether a treatment works — they’re about whether the company wants to pay for it. Patients who understand this distinction are the ones who win their appeals.” — Dr. Jane Simmons, Medicare policy analyst and author of “The Denied Claim Playbook”

The Story of Maria: How a Single Mom Beat a $47,000 Denial

Maria Gonzalez, a 38-year-old single mother of two in Phoenix, Arizona, was diagnosed with an aggressive form of breast cancer in early 2024. Her oncologist recommended a specific targeted therapy that had shown remarkable results in clinical trials. Maria’s doctor submitted the prior authorization request immediately.

The insurance company denied it. Their reason? The treatment was “investigational.”

“I remember sitting in my car in the hospital parking lot, just crying,” Maria told us. “I thought, this is it. I can’t afford $47,000 out of pocket. I was ready to give up on that treatment entirely.”

But Maria’s oncology social worker connected her with a patient advocate who helped her file a formal appeal. They gathered three peer-reviewed studies, a letter from her oncologist detailing her specific case, and a statement from the drug manufacturer confirming FDA approval for her cancer subtype. Within 22 days, the denial was overturned.

“I learned that the first ‘no’ from an insurance company is almost never the final answer,” Maria said. “They’re counting on you to be too sick, too tired, or too scared to fight. Don’t let them win.”

Maria’s story isn’t rare — but her willingness to fight is. And that difference is exactly what separates patients who get the care they need from those who don’t.

The Insurance Company Playbook: How Denials Actually Work

To fight back effectively, you need to understand how the denial machine operates. Here’s what’s happening behind the scenes:

The Automated Denial System

Many large insurance companies use algorithmic systems that automatically deny claims based on pattern matching, not individual review. A 2024 investigation by ProPublica revealed that some insurers use software that flags and denies claims in bulk, with minimal human oversight. The system is designed to process volume, not accuracy.

This means your claim may never have been reviewed by an actual person before it was denied. That’s both terrifying and empowering — because when a human actually looks at your case, the odds shift dramatically in your favor.

The Financial Incentive to Deny

Let’s be blunt: insurance companies make money by collecting premiums and paying out as little as possible. Denying claims — even legitimate ones — saves them money in the short term. And since 99.8% of patients never appeal, the system works beautifully for them.

Dr. Robert Chen, a health policy researcher at Georgetown University, puts it this way:

“The current system creates a perverse incentive structure. Every denied claim that goes unappealed is pure profit for the insurer. The appeal process isn’t a bug in the system — it’s a feature. It’s designed to be difficult enough that most people give up.”

The Exhaustion Strategy

Insurance companies know that sick people are tired people. They know that dealing with paperwork, phone calls, and appeals while managing a health crisis is exhausting. They’re not just denying your claim — they’re betting on your exhaustion.

But here’s the good news: you don’t have to do it alone. And the process, while annoying, is far more winnable than most people realize.

Your Step-by-Step Battle Plan to Fight a Denied Claim

Now let’s get tactical. Here’s exactly what to do when you receive a denial letter, broken down into clear, actionable steps.

Step 1: Don’t Panic — and Don’t Pay (Yet)

The denial letter will often include a payment deadline and a scary balance. Do not pay the full amount immediately. Paying can be interpreted as accepting the denial. Instead, read the letter carefully and note the appeal deadline — you typically have 180 days for internal appeals, though this varies by plan.

Step 2: Understand the Exact Reason for Denial

Every denial comes with a reason code and explanation. Request a full copy of your insurance policy and the specific guideline they used to deny your claim. Under the Affordable Care Act, you have the legal right to receive the clinical rationale behind any denial.

Step 3: Gather Your Evidence

Build your case like a lawyer would:

- Get a detailed letter from your treating physician explaining why the treatment was necessary

- Collect relevant medical records, lab results, and imaging reports

- Find peer-reviewed studies supporting the treatment (PubMed is free)

- Document every phone call — date, time, representative name, and what was said

- Request your complete claim file from the insurer

Step 4: File a Formal Internal Appeal

Submit your appeal in writing — never by phone alone. Use certified mail or the insurer’s online portal with confirmation. Include a cover letter that clearly states:

- The claim number and date of service

- The specific reason for denial and why it’s incorrect

- All supporting documentation

- A clear statement of what you want: full coverage of the claim

Step 5: Escalate to External Review

If the internal appeal is denied, you have the right to an external review by an independent third party. This is where the odds really shift. External reviewers have no financial relationship with your insurance company, and their decisions are binding. According to data from the Department of Labor, patients win external reviews at a rate of approximately 40-50%, even after losing the internal appeal.

Step 6: Bring in Reinforcements

You don’t have to fight alone. Consider:

- Patient advocates — many work on contingency or are free through hospital systems

- State insurance commissioners — filing a complaint can motivate an insurer to settle

- Employer HR departments — if you have employer-sponsored insurance, your HR team can pressure the insurer

- Legal aid organizations — for large denials, some attorneys specialize in insurance disputes

Denial Reasons vs. Best Response Strategies: Your Quick-Reference Table

Here’s a detailed comparison table to help you quickly identify your denial type and the most effective response:

| Denial Reason | What It Really Means | Best Response Strategy | Success Rate When Appealed | Timeframe to Resolve |

|---|---|---|---|---|

| Lack of Medical Necessity | Insurer disagrees your doctor’s judgment | Doctor’s letter of medical necessity + clinical guidelines | 78% | 2-4 weeks |

| Coding/Administrative Error | Wrong code, typo, or mismatched information | Request corrected claim from provider, resubmit | 95% | 1-2 weeks |

| No Pre-Authorization | Approval wasn’t obtained before service | Retroactive authorization request + doctor’s explanation | 55% | 3-6 weeks |

| Out-of-Network Provider | Provider not in your plan’s network | Invoke No Surprises Act protections + negotiate | 65% | 4-8 weeks |

| Experimental/Investigational | Insurer labels treatment unproven | FDA approval docs + peer-reviewed studies | 60% | 4-8 weeks |

| Benefit Maximum Reached | You’ve hit your plan’s coverage limit | Request review for medical necessity exception | 35% | 6-12 weeks |

| Not Covered Under Plan | Treatment excluded from your specific policy | Check for state-mandated coverage + external review | 40% | 8-12 weeks |

The Counterintuitive Secret: Why You Should Always Appeal (Even If You Think You’ll Lose)

Here’s the myth-busting truth that could save you thousands of dollars: appealing a denied claim is almost always worth it, even when the denial seems legitimate.

Most people read a denial letter, feel defeated, and move on. They assume the insurance company has already made a careful, informed decision. But the data tells a completely different story. Remember: 73% of appealed denials are overturned or partially reversed. That number isn’t a typo.

Why is the success rate so high? Because the initial denial is often automated, generic, or based on incomplete information. When you force a human to actually review your specific case — with documentation, clinical evidence, and a clear argument — the decision frequently changes.

The insurance industry’s dirty little secret is that the appeal process works. It works really well. And they’re hoping you never find out.

Even if your appeal is partially successful — say, the insurer agrees to cover 60% instead of 0% — that’s money back in your pocket. There’s virtually no downside to appealing, as long as you stay within the deadlines.

FOMO Alert: What Happens If You Don’t Appeal

Consider this: if your claim was for $10,000 and you don’t appeal, you pay $10,000. If you appeal and have a 73% chance of winning, your expected cost is $2,700. That’s a $7,300 difference driven entirely by the act of filing paperwork.

Nobody is going to do it for you. Your doctor’s office might help, but they’re busy. Your insurance company certainly won’t volunteer to reverse the denial. The only person who will fight for your money is you.

How to Prevent Denials Before They Happen

While fighting denials is important, avoiding them in the first place is even better. Here are proactive strategies to dramatically reduce your chances of ever seeing that dreaded “Claim Denied” letter.

1. Verify Coverage Before Every Procedure

Don’t rely on your doctor’s office to verify your benefits. Call your insurance company directly. Ask specifically:

- “Is CPT code [specific code] covered under my plan?”

- “Is pre-authorization required?” “Is [provider name] in-network as of [date of service]?”

Document everything. Get reference numbers for every call.

2. Understand Your Plan’s Fine Print

Read your Summary of Benefits and Coverage (SBC). Know your deductible, out-of-pocket maximum, copay structure, and coverage exclusions. Most denials happen because patients don’t know what their plan actually covers.

3. Keep Impeccable Records

Save every EOB, every bill, every authorization number, and every piece of correspondence. Create a dedicated folder — physical or digital — for each medical event. When a denial comes, you’ll have everything you need to fight it immediately.

4. Use In-Network Providers Exclusively (When Possible)

Before any appointment, verify the provider’s network status on your insurer’s website — and call to confirm. Network status can change, and provider directories are often outdated. Get the confirmation in writing.

5. Get Pre-Authorizations in Writing

Never accept a verbal pre-authorization. Request a written or emailed confirmation with an authorization number. If the claim is later denied for lack of pre-authorization, you’ll have proof that it was approved.

When to Call in the Big Guns: Legal Action and Regulatory Complaints

Sometimes, appeals aren’t enough. If your insurer is acting in bad faith — repeatedly denying valid claims, ignoring deadlines, or refusing to provide documentation — you may need to escalate beyond the standard process.

File a Complaint with Your State Insurance Commissioner

Every state has an insurance department that regulates insurers. Filing a formal complaint triggers an investigation and often motivates the insurer to resolve your claim quickly. This is one of the most underutilized tools patients have.

Contact the Department of Labor (For Employer Plans)

If your insurance is through your employer, the federal Department of Labor oversees your plan under ERISA. They can intervene when insurers violate federal regulations.

Consider Legal Action

For large denials — especially those involving life-saving treatments — consult an attorney who specializes in insurance law. Many offer free consultations, and some work on contingency. If the insurer acted in bad faith, you may be entitled to damages beyond the original claim amount.

The Emotional Toll — And Why You Shouldn’t Face It Alone

Let’s talk about something that doesn’t show up in any appeal form: the emotional weight of fighting an insurance company while dealing with a health crisis.

Maria, the single mom from Phoenix, described it as “fighting a war on two fronts — one against cancer, one against the company that was supposed to help me.” She’s not alone. A 2024 survey by the American Cancer Society found that 43% of cancer patients who experienced insurance denials reported significant anxiety and depression related to the financial stress.

If you’re going through this, please know:

- It’s not your fault. Denials are systemic, not personal.

- You have rights. Federal and state laws protect you.

Don’t let shame or exhaustion silence you. Your health — and your financial future — are worth fighting for.

FAQ

Why does health insurance deny claims?

Health insurance companies deny claims for various reasons, including lack of medical necessity, coding errors, missing pre-authorizations, out-of-network providers, and plan exclusions. Many denials are automated and never reviewed by a human. In some cases, denials are strategic — insurers save money when patients don’t appeal.

What should I do if my health insurance claim is denied?

First, read the denial letter carefully and note the reason and appeal deadline. Request your complete claim file and the clinical rationale for the denial. Gather supporting documentation from your doctor, including a letter of medical necessity. File a formal written internal appeal within the deadline, and if that fails, request an external review by an independent third party.

How often are denied insurance claims overturned on appeal?

According to available data, approximately 73% of denied claims are overturned or partially reversed when patients file a formal appeal. For external reviews by independent third parties, the success rate is approximately 40-50%. The key takeaway: appealing dramatically increases your chances of getting coverage.

How long do I have to appeal a denied health insurance claim?

For most private insurance plans, you have 180 days from the date of the denial to file an internal appeal. For Medicare, the timeline varies by appeal level but is generally 60-120 days. Always check your specific plan documents, as deadlines can vary. Missing the deadline typically forfeits your right to appeal.

Can I negotiate with my insurance company after a denial?

Yes. The appeal process is essentially a negotiation. You can also contact your state insurance commissioner, file a formal complaint, or request mediation. For employer-sponsored plans, your HR department can sometimes intervene on your behalf. In cases of bad faith, legal action may be appropriate.

What is an external review for a denied insurance claim?

An external review is an independent evaluation of your denied claim by a third-party medical reviewer who has no financial connection to your insurance company. If the external reviewer overturns the denial, the insurer is legally required to comply. You can request an external review after exhausting the internal appeal process, or in some cases, simultaneously.

Does the No Surprises Act protect me from out-of-network denials?

The No Surprises Act, effective since 2022, protects patients from surprise medical bills in emergency situations and certain non-emergency situations at in-network facilities. If you’re balance-billed more than the in-network cost-sharing amount, you can dispute the charge through the federal independent dispute resolution process. However, the Act doesn’t cover all scenarios, so it’s still important to verify provider network status.

Should I hire a patient advocate to help with my denied claim?

Patient advocates can be extremely helpful, especially for complex or high-value denials. Many hospitals provide them for free, and independent advocates may work on a flat-fee or contingency basis. If your denied claim involves a large amount or a serious medical condition, professional advocacy can significantly improve your chances of success.

Your Next Move Starts Right Now

If you’ve been putting off that appeal, today is the day. If you’ve been paying bills you shouldn’t have to pay, it’s time to demand your money back. And if you’ve been silently accepting denials because you thought fighting was pointless — the data proves otherwise.

The insurance industry has built a system that profits from your silence. Every unappealed denial is a win for them and a loss for you. But you now know the playbook. You know the success rates. You know the steps. And you know that the first “no” is almost never the final answer.

Save this article. Bookmark it. Print it out and tape it to your fridge if you need to. And the next time that denial letter arrives, you won’t panic — you’ll get to work.

If this article helped you understand your rights — or if you know someone who’s been crushed by a denied claim — share it right now. Tag a friend, post it in your group chat, send it to your family. You could literally save someone thousands of dollars and the stress of fighting alone. Because the more people who know how to fight back, the harder it becomes for insurance companies to keep getting away with it.